The signal improved, but it is not simple

Manufacturing gave equipment buyers a stronger signal this week, but not a simple one.

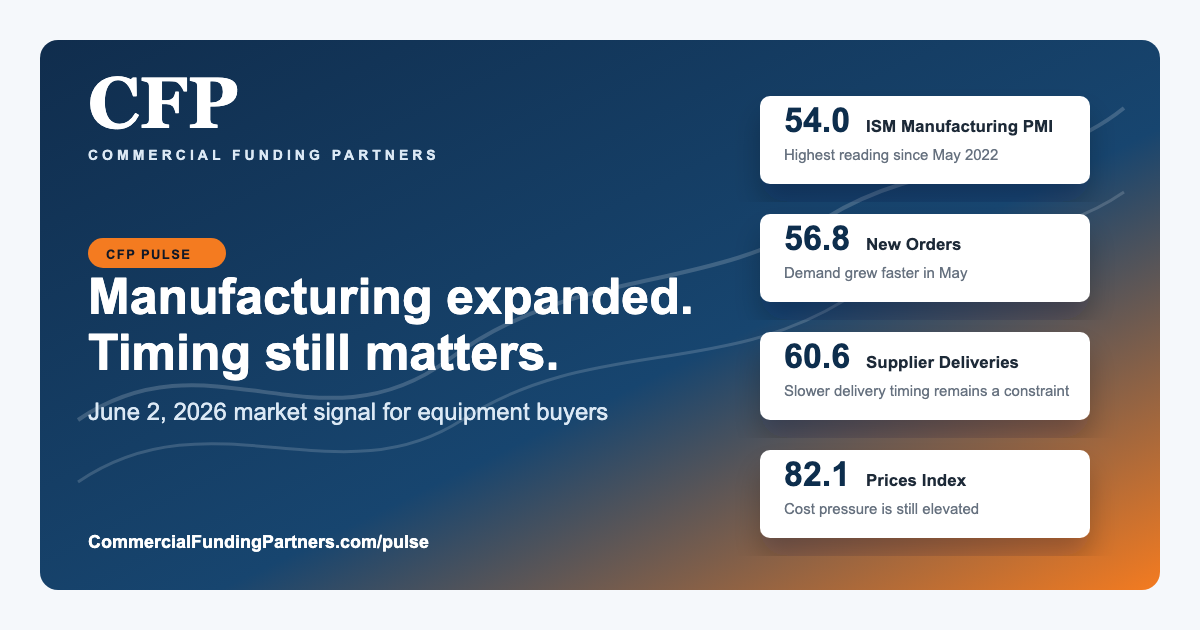

The latest ISM Manufacturing PMI report showed U.S. manufacturing expanding again in May. The headline PMI registered 54.0, up from 52.7 in April, and ISM noted that it was the highest reading since May 2022. New orders rose to 56.8, production rose to 54.3, and backlog of orders moved further into expansion at 52.2.

That is useful news for companies considering equipment, capacity, automation, fleet, or production investments. It suggests buyers are not just planning in theory. More orders and more production usually create real pressure to add capability.

The operating detail still matters

ISM’s Supplier Deliveries Index remained at 60.6. In that index, a reading above 50 indicates slower deliveries. Prices also remained elevated at 82.1, even though the index eased from April. ISM also reported customer inventories were still “too low,” a signal that future production needs may remain active.

For equipment buyers, the practical takeaway is not “go faster at any cost.” It is: if the project is moving, make sure the financing structure matches how the project will actually unfold.

The Census Bureau’s latest durable goods advance report points in the same direction. April new orders for manufactured durable goods increased 7.9% to $346.0 billion. Excluding transportation, new orders increased 1.1%. Unfilled orders rose 1.7% to $1.569 trillion. That does not mean every sector is moving the same way, but it does show why equipment timing, backlog, supplier readiness, and purchase sequencing matter.

Where standard financing can get too narrow

A clean invoice-and-delivery loan may work when the machine is available, the vendor payment is simple, and the borrower only needs funding at delivery. Many real projects are not that clean.

Structure friction often shows up when a buyer has

- vendor deposits or progress payments before delivery,

- imported or specialized equipment,

- a long delivery or installation window,

- multiple assets across multiple locations,

- bank hold or collateral limits,

- rising input costs that pressure working capital, or

- a project that must start before the equipment is fully producing.

Why it matters

Those are not just documentation details. They affect how cash leaves the business, when collateral exists, when the equipment can support revenue, and whether the borrower has enough liquidity to keep the rest of the operation moving.

Where CFP can help

Commercial Funding Partners is most relevant when the financing conversation needs to follow the project plan, not just the quote. That can include equipment financing, sale-leaseback, tax-lease structures, progress funding, multi-entity transactions, and specialized equipment situations where the bank path is too slow, too narrow, or already at its limit.

The better move is to bring the financing conversation forward. Before the purchase order is final, before deposit dates are locked, and before the delivery schedule creates pressure, buyers should understand how the capital structure will support the whole project.

Related proof

See CFP’s equipment-financing case studies.

Previous Pulse

Read the June 1 brief on equipment-finance demand and structure.

Source notes: ISM May 2026 Manufacturing PMI report and U.S. Census Bureau April 2026 Durable Goods Advance Report.